Investors have to decide how much to withdraw, and are caught between the fear of outliving their funds or delaying joy too much

HOW would you like a retirement investment vehicle that is liquid, has no maturity date, and automatically adjusts your asset allocation even well into retirement?

To be sure, there is no shortage of funds to select from for a retirement portfolio. But unless you have an adviser, you will need to monitor the asset allocation regularly to ensure it remains suitable for your investment horizon. You will also need to choose from among the bewildering array of funds in the market.

In terms of asset allocation, conventional wisdom says the closer you get to retirement, the more conservative your portfolio should become. A higher fixed income allocation close to or in retirement helps to cushion against a sharp equity downturn. It also provides stability as you begin to draw on your portfolio for income.

Glidepath funds, which mechanically adjust your asset allocation with age, offers simplicity and convenience in a single vehicle. Investing regularly in such a fund also mitigates your worst impulses, such as panic selling in a downturn.

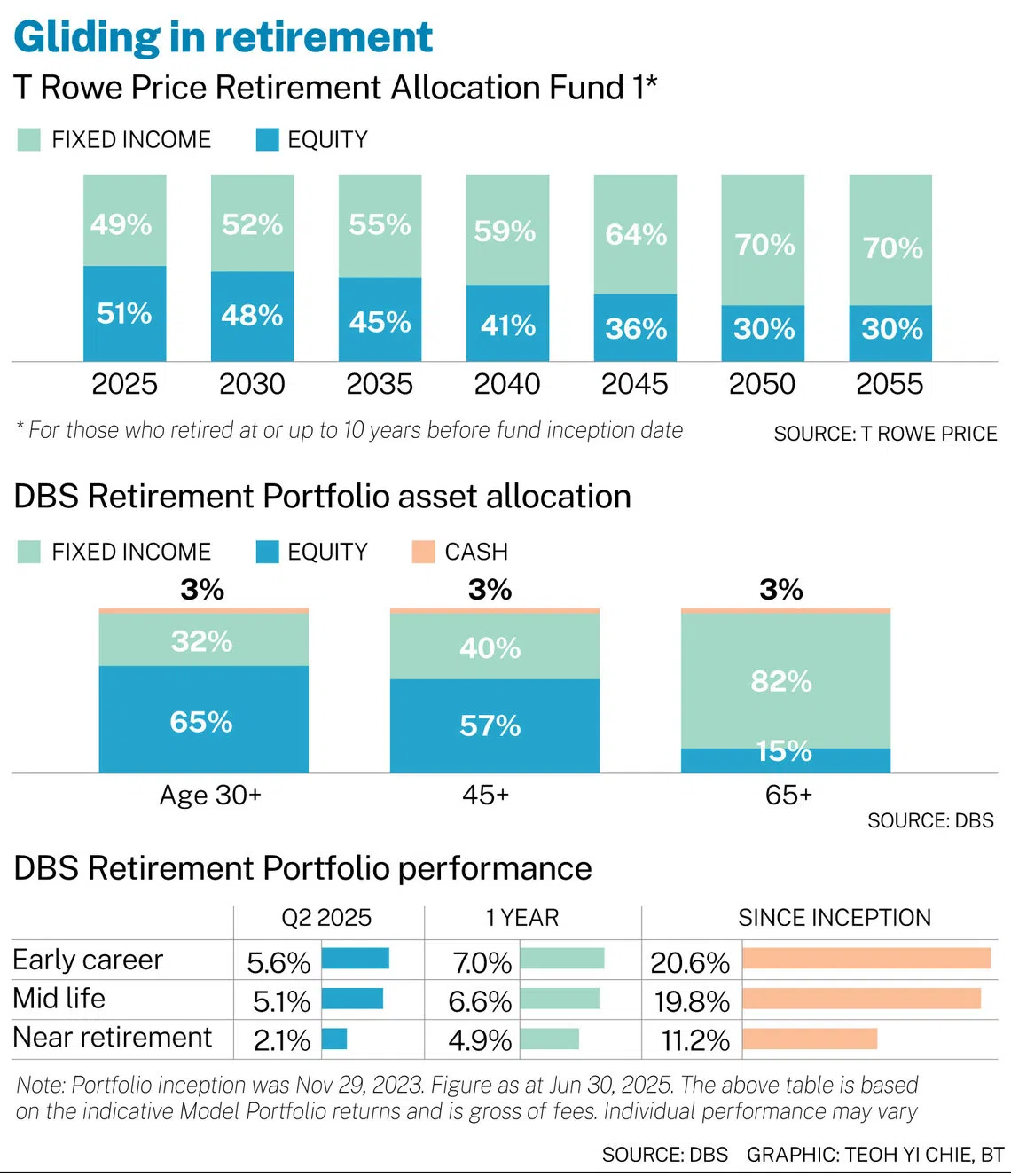

Two new glidepath funds were recently rolled out by T. Rowe Price and HSBC – the T Rowe Price Retirement Allocation Fund 1 and 2.

The products are the second glidepath offering in the market. The first came from DBS Bank, which, in partnership with JPMorgan Asset Management (JPMAM), rolled out the Retirement Portfolio last year. The portfolio sits within the DBS digibank app.

BT in your inbox

Start and end each day with the latest news stories and analyses delivered straight to your inbox.

DBS says it sees “healthy interest” in the Retirement Portfolio. The number of investors has grown more than five times to date since the start of the year. Around 7 per cent of investors are in the withdrawal or decumulation phase.

Decumulation, the stage when you begin to withdraw from your portfolio for expenses in retirement, remains a big gap in the marketplace. There are investment-linked insurance plans (ILPs) that can pay a fixed income in retirement, but you would have to reckon with the high costs of an ILP wrapper.

The challenge in decumulation is this: How do you go about deciding how much to withdraw to make your savings last as long as possible?

SEE ALSO

Longevity means you could outlive your funds. A higher cost of living, coupled with a fall in your portfolio value, could also burn a hole in your finances.

For two years running, BlackRock’s chief executive Larry Fink, in his annual letters to shareholders, has lamented that retirees struggle with the puzzle of longevity and how much to withdraw from their savings. “A 401(k) doesn’t come with instructions. When you retire, you’re handed a lump sum and asked to make it last for the rest of your life – without knowing how long that will be.

“The result? Even retirees who have saved well often spend too little, gripped by fear that they would run out. They downsize dreams and delay joy. The economist Bill Sharpe called this problem the ‘nastiest, hardest problem in finance’.”

Morningstar in its latest retirement income report posits that the “safe” withdrawal rate for a balanced portfolio over 30 years is 3.7 per cent for portfolios between 20 and 50 per cent in equities. In 2023, the safe withdrawal rate for a 40 per cent equity/60 per cent bond portfolio was 4 per cent.

While the report is US-centric, there are some insights that can apply in the Singapore context. Morningstar, for instance, suggests US savers delay their Social Security payouts. Singaporeans have the CPF Life, which pays an income for life and is widely seen as the backbone of a retirement income plan, augmenting other sources of income. It is one of a few variables that retirees could adjust. CPF Life payouts may start at 65. Or, you could delay the payouts up to age 70, and rely more on your personal savings in the interim.

Morningstar also posits the concept of “dynamic” withdrawals, where a retiree could adjust his withdrawals based on portfolio performance. “Flexible strategies are effective because they help to prevent retirees from overspending in periods of market weakness, while giving them a raise in stronger market environments.”

Nick Tong, T Rowe Price’s head of South-east Asia intermediary distribution, noted that investors are often paralysed by the question of how much to withdraw. “We believe this paralysis is often due to a lack of a structured plan and uncertainty about how their savings will perform under different market conditions.

“Our approach emphasises the importance of having a comprehensive plan and regularly stress-testing it against real-world scenarios… based on various withdrawal rates, market returns and life expectancy assumptions.”

The new T Rowe Price glidepath funds have a distribution share class (in US dollars or Singapore dollars) of 6 per cent, which means there is no flexibility to adjust the payout rate. You should note, too, that the distribution may comprise income, capital gains and capital itself. “Any charges or dividend distributions paid from capital can result in capital erosion and constrain capital growth,” says the funds’ product highlight sheets.

HSBC, which is for now the exclusive distributor, said: “There is no pre-set or modelled withdrawal mechanism – investors retain full flexibility to redeem their holdings at any time…”

In contrast, DBS’ Retirement Portfolio relies on a robo to enable investors to customise their withdrawals and retirement date. The app takes the withdrawal rate and models it against return assumptions to tell you how long your kitty can last. You can also input your own inflation assumption.

Here are a couple of other differences between the T Rowe Price and DBS offerings:

• Fund format vs managed portfolio. The T Rowe Price products are discrete funds, and their investors become part of a cohort. Fund 1 is for those who retired at or up to 10 years before the fund’s inception. In 2025, the asset mix begins at 51 per cent equities, 49 per cent fixed income. Fund 2 is for those who will retire within 10 years of the fund’s inception. The allocation starts at 65 per cent equity, 35 per cent fixed income.

In contrast, DBS’ Retirement Portfolio is a managed portfolio. Your asset allocation is determined by your own desired retirement date, and can be amended anytime. Your funds will be allocated into specific JPMAM funds comprising four equity funds (US, Europe, Asia, Japan) and three fixed income funds (government bonds, corporate bonds, emerging market debt).

• Fees. The T Rowe Price funds charge up to 1 per cent in annual management fee. DBS’ Retirement Portfolio charges 0.75 per cent a year in the accumulation phase. This dials down to 0.25 per cent in the retirement phase. There is no early withdrawal penalty or lock-in period.