Most people don’t struggle with money because they are careless. They struggle because spending decisions happen quietly every day. A food order here, an unplanned purchase there, and by month-end the budget feels tight. That is why expense reduction works best when we improve habits, not when we attempt extreme cuts for a few days.

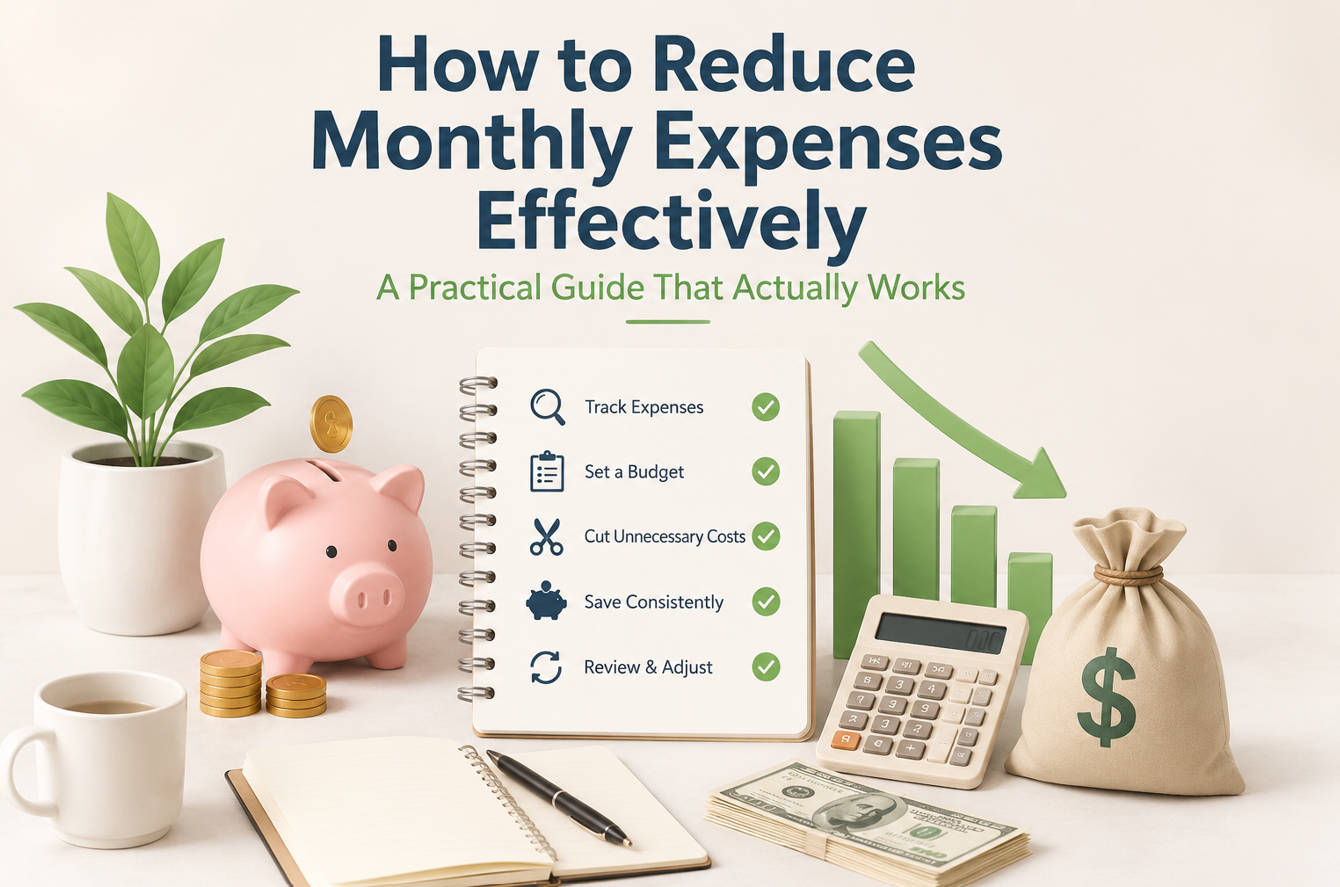

Start by Tracking Before Cutting

If you want real improvement, begin with one month of honest tracking. Don’t overthink it. Just note every expense. Once this is done, patterns become obvious. Many people find that major expenses are not the problem rather repeated unaccounted small transactions are the real issues. This one step alone changes financial awareness and creates a strong base for better decisions.

Separate Essentials needs, Lifestyle, and Waste expenses

After tracking, divide your spending into three simple groups which are essentials, lifestyle choices, and avoidable waste. Essential things are those which are unavoidable and include rent, groceries, utility bills, school and transport expenses.

Lifestyle choices include the expenses on dining, shopping, and entertainment. Waste expense is where the biggest savings usually spent, such as unused subscriptions, duplicate plans, and impulse purchases. We should look to reduce waste which first gives quick results without feeling painful.

Use a Budget Framework That Feels Practical

A simple structure like the 50/30/20 rule can help many beginners. You can see this as a direction, rather than a hard and fast rule to follow. If your fixed costs are currently high, start with a custom split and improve month by month. Consistency matters far more than perfection. The main goal of this is to keep spending under control while slowly increasing savings.

Focus on the Bigger Expense Categories

Meaningful savings starts when you work to control on your biggest monthly expenses first. Housing costs can often be optimized through rent discussions or utility discipline. Food spending can drop when weekly planning replaces frequent delivery habits. Transport costs improve when commute decisions become intentional. Debt pressure reduces when high-interest liabilities are handled first. Unnecessary subscription cleanup is also powerful because these charges repeat silently every month which can save you some money from this.

Automate Savings and Add Spending Friction

One of the most effective habits is to save first, not at last. You can set an automatic transfer as soon as income deposits in your account or comes to your hands. This builds discipline naturally. Alongside this, reduce impulse spending by adding small friction. A 24-hour pause before non-essential purchases, removing saved cards from shopping apps, and using spend alerts can significantly reduce unnecessary outflow.

Renegotiate Monthly Bills Regularly

Many people overpay on mobile, broadband, and digital services simply because old plans continue by default. A quick review or negotiation can lower recurring costs. Even small monthly reductions create meaningful annual savings. This strategy is especially useful because it doesn’t require cutting quality of life.

Keep the Plan Human and Sustainable

If you manage household expenses with a partner or family, regular communication is important. A short monthly review helps identify overspending and prevents confusion. The most successful plans are simple enough to continue for years. A strict plan that breaks in two weeks is less useful than a realistic plan that lasts.

Guard Against Lifestyle Inflation

As income rises, spending often rises automatically. That habit can quietly erase progress. A better approach is to increase your savings rate first whenever income grows, then upgrade lifestyle gradually. This keeps financial growth stable while still allowing better living standards.

Conclusion

Reducing monthly expenses effectively is not about living with constant restrictions. It is about spending wherever is necessary. When you track your input/inflow and output/outflow of money clearly, cut waste first, automate savings, and review regularly, money stress begins to fall. Over time, these small systems create bigger confidence, stronger savings, and better long-term financial stability.

Related

Discover more from Newskart

Subscribe to get the latest posts sent to your email.